A preference share is a hybrid instrument possessing features of both common shares and debt. When it

has convertibility features, (it is converted to a pre-determined number of common stocks in future), it tends to exhibit common stock performance. But in the case of the Coreshares Preftrax ETF – where the fund carries fairly plain preference stocks without such exotic features – performance is similar to a debt instrument.

It derives value primarily from its coupon rate (and dividend yield) relative to prevailing market interest rates. This means, like other debt instruments, it has limited upside potential and is held by investors mainly for income generation. For the most part then, the fund needs to be evaluated relative to other fixed-interest instruments such as bonds.

The coupon rate is a predetermined rate based on par or face value, which is used to calculate the dividend that an investor will receive – calculated as the coupon rate multiplied by par value. For instance, if the par value is R1,000 and the coupon rate is 7%, it means the investor receives R70 annually in dividends. However, the dividend yield is based on the market price of the preference share, that is, the dividend received divided by the market price.

Click logo to view

CoreShares PrefTrax ETF on EasyEquities

Let’s say the price of the preference share has deviated from its par value to R950 – then the dividend yield will translate to 7.4%. All other things being equal, as market interest rates increase, the price of preference shares decrease because investors sell preference shares and buy new, higher yielding instruments – and this pushes the price of preference shares down. The opposite happens when yields fall or are expected to decline.

Fund description: CoreShares PrefTrax tracks the FTSE/JSE preference share index which measures the performance of nonconvertible, floating rate perpetual preference shares (these are the most standard form of preference share which cannot be converted to ordinary equity or be recalled by the company).

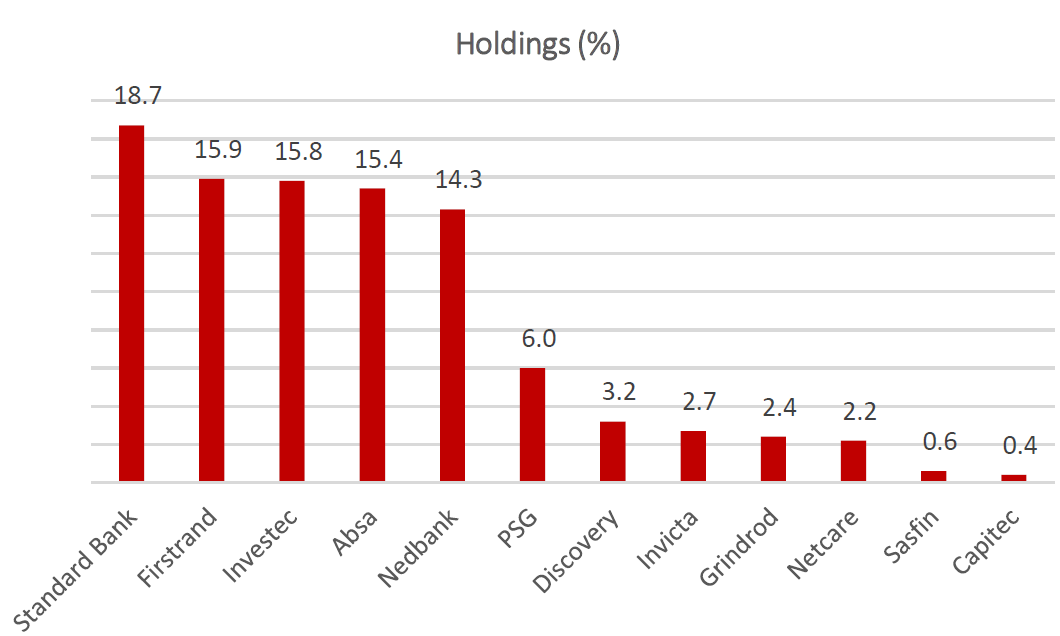

Top holdings: Banks command the lion’s share of 89.4% of the preference equity fund.

Suitability: CoreShares PrefTrax shares is likely to appeal to high net worth, income-focused investors. In SA, a dividend withholding tax of 20% is paid on dividends earned from preference shares, giving them a tax advantage over bonds and money market instruments which are taxed at the marginal income tax rate of the taxpayer once the interest exemption of R23,800 (or R34,500 if investor is over 65 years) is used up. Share capital appreciation is limited, so when investing in this ETF your main aim should be to generate income. Trading in the ETF, as opposed to the underlying preferences shares, affords improved liquidity, which is guaranteed by the market maker, Sanlam Private Wealth.

Historical performance:

Net asset value performance to end-June 2019 in percentages (annualised for periods over one year)

The Coreshares Prefetrax fund has performed exceptionally well in the 12 months to end-June, ahead of both the all share and bond indices, helped by strong price gains off a low base. The fund’s share price struggled in the first six months of last year, where it recorded its lowest price point since its inception in 2012. However, its three- and five-year annualised returns are in line with the Newfunds Govi ETF which houses nominal government bonds. (Return is derived from adding price changes and dividend received).

Fundamentals: The receipt of the fund’s preference dividend is highly probable because most of the issuers are reputable institutions that have managed to grow profits, albeit marginally, under today’s difficult economic conditions. South African banks make up more than 89% of the fund’s holdings. However, if the economy remains under strain it could adversely affect their ability to pay preference dividends in future. It is important to note that companies have no obligation to pay out preference dividends. This is one of the fund’s primary disadvantages – while it has ordinary equity downside risks, it does not have the same unlimited upside potential. For this reason, the fund is more attractive if it offers an after-tax yield that is higher than bonds to compensate for the elevated risk.

Click logo to view

CoreShares PrefTrax ETF on EasyEquities

Historically, South African preference shares have outperformed bonds on an after-tax yield basis – given the tax benefit outlined above. The Coreshares Preftrax fund manager says the ETF has historically performed better than a composite of government bonds on an after-tax yield basis by an average of 3.4 percentage points. Moody’s – the only ratings agency still holding SA sovereign debt as investment grade – says the latest R59bn Eskom bailout by government is credit negative, which increases the risk of a downgrade to junk.

If Moody’s downgrades SA’s debt, borrowing costs will rise as we are likely to experience an outflow of approximately $14bn (R200bn) from the economy. This is because South African government bonds will fall out of Citibank’s global bond index which holds only investment-grade debt, and certain fund managers are mandated to hold investment-grade debt only in their portfolios. The ensuing rising cost of debt (or yield) could see preference shares lose value as investors move to higher-yielding bonds.

Additionally, ratings agency Fitch – which already has SA debt as sub-investment grade – has downgraded SA’s economic outlook to negative from stable, pushing it further into junk territory. Finally, the recent cut in SA’s prime interest rate reduces the yield of preference shares, given they have floating coupon rates based on the prime lending rate. Countering that, the yield on government bonds is expected to increase, which could reduce the value and appeal of preference shares.

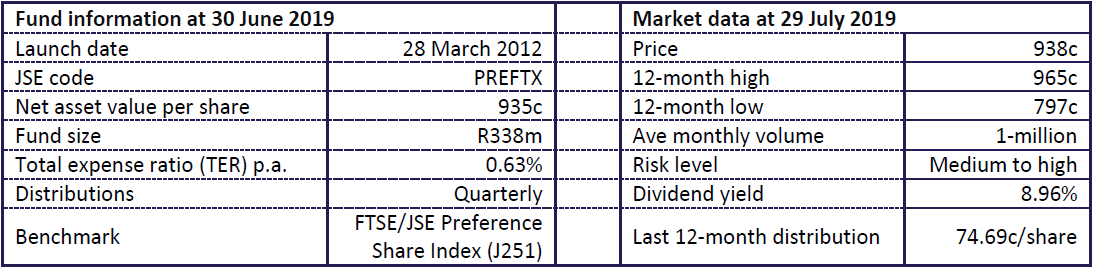

Fund statistics:

Alternatives: There are no direct peers. However, given that the CoreShares PrefTrax ETF derives the bulk of its value from interest rate movements, the Newfunds Govi ETF (TER: 0.34%) is its distant cousin.

Click logo to view

CoreShares PrefTrax ETF on EasyEquities

Background: Exchange-traded funds (ETFs)

Exchange-traded funds (ETFs) are passively managed investment funds that track the performance of a basket of pre-determined assets. They are traded the same way as shares and the main difference is that whereas one share gives exposure to one company, an ETF gives exposure to numerous companies in a single transaction. ETFs can be traded through your broker in the same way as shares, say, on the EasyEquities platform. In addition, they qualify for the tax-free savings account, where both capital and income gains accumulate tax free.

Benefits of ETFs

- Gain instant exposure to various underlying shares or bonds in one transaction

- They diversify risk because a single ETF holds various shares

- They are cost-effective

- They are liquid – it is usually easy to find a buyer or seller and they trade just like shares

- High transparency through daily published index constituents

Intellidex reviews:

Ashburton Global 1200 ETF

|