Take a listen to Mark's thoughts here.

Energy

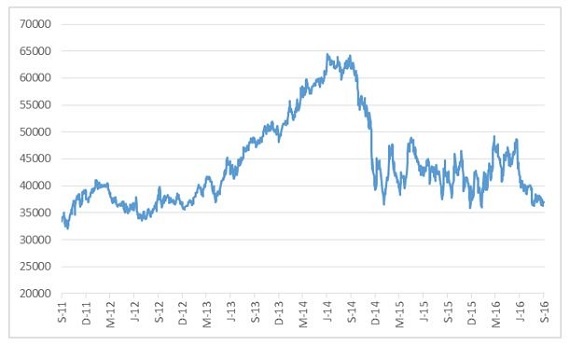

Share price: R370,30

Net shares in issue: 610,6 million

Market cap: R226,1 billion

Exit PE ratio 9,3x; forward PE 10,9x; dividend yield 4,0%

Fair value: R440

Target price: R580

Trading Buy and Portfolio Buy

Key takeaway:

Annual earnings are out and, as expected, are down. For a number of months now I’ve forecast a 21% drop in earnings per share, from 4976 cents to 3912 cents. The trading statement on the 6th of June indicating a 10% to 30% drop squares with this expectation, so no surprises. In practice, HEPS is down by 17% to 4140 cents. Earnings per share is 56% down, largely due to a shale gas impairment of R10 billion, of which R7,4 billion came through in H1. I currently estimate earnings will be down again in F2017 by 18% to 3400 cents before recovering in F2018 to 3865 cents. This is subject to revision following analysis of the F2016 result and management feedback. Sasol declared a final dividend of 910 cents (higher than my estimate of 830 cents) making for a full year dividend of 1480 cents, down 20%.

Recommendation:

Whilst earnings are down this is no reason to panic. Sasol’s earnings can be all over the place because of the ups and downs of oil, currency and chemicals prices and volumes produced. This is a complex beast. The monster Lake Charles project in Louisiana and the implications of that aside, the stock is fundamentally on the cheap side even allowing for a soggy earnings picture. Cash flow is positive, the debt to equity ratio is 14% and the balance sheet can take the big capex strain for the next two years with debt to equity peaking at below 50%.

I have kept Sasol a trading Buy with the caveat of selling the rallies into strength, as the catalysts for a sustained bull phase are not there. Weakness below R400 remains an opportunity.

Fair value at R440 with target price maintained at R580 on a positive fundamental longer run outlook.

Here are a few things to take note of in the official figures.

The average rand dollar exchange rate for F2016 is R14,52/$ compared with R11,45/$.

The oil price is 41% lower at an average of $43,37/bbl.

Earnings are affected by the reversal of a tax provision in Nigeria worth R2,3 billion or 377 cents per share and a R1 billion currency translation gain.

Refining margins are lower in dollars but petrol crack spreads are higher on average whilst diesel crack spreads are lower.

Petrol prices were 15% lower in F2016 in ZAR whilst diesel prices are 25% lower.

Refining margin for F2016 are slightly higher at $14/bbl.

Polymer prices are down sharply in USD with propylene down 33%, polypropylene down 25% and low density polyethylene and linear low density polyethylene down 15% each. Coal is about 17% lower on average.

A $1/bbl change in the petrol crack spread has about a 65 cents per share impact on EPS whilst a $1/bbl change in the diesel crack spread has a 50 cents EPS impact for a combined 115 cents impact.

Energy is the largest contributor at 43% of clean operating profit even though profits are down by 28%.

Base Chemicals profits are down by 44%. However, both Performance Chemicals and Mining are above their 2015 level.

The decline in the group operating profit, before translation gains/losses and remeasurement items, is limited to 23%.

The approval by the National Energy Regulator of increased tariffs on the Transnet liquid fuel pipeline will positively affect Sasol earnings by R200 million in year one and R500 million thereafter.

On balance, not a bad result in the conditions.

A few thoughts on Lake Charles, which I visited on my trip to Houston last year.

The Lake Charles Chemical Project in Louisiana will cost more than originally projected with the capital costs moved out by 20% to about $11 billion or an extra $2 billion. However, in an earlier note I observed that “cost-creep is a common feature of such mega-projects and I have little doubt that over the build horizon we should prepare for that to edge up.”

The economics of Lake Charles are much more sensitive to chemical prices than capital costs – in other words oil, gas, ethane, and ethylene spreads, inter alia. An abundance of low-cost feedstock will make Sasol less sensitive to the traditional oil and currency dynamics - earnings diversification results in those old correlations becoming far less pronounced.

The NPV of Lake Charles in a static modelling scenario would reduce but I’ve been conservative and at this point keep the PV unchanged at R65 per share with additional EPS at around R12. IRR of around 8,5% is in line with cost of capital. Time will tell – the chemicals project will start to contribute materially to earnings only from F2019/F2020.

Whilst oil and the rand/dollar exchange rate are the two key variables driving earnings, this sensitivity is less pronounced should the Lake Charles chemicals project realises its anticipated benefits.

I estimate Lake Charles could reduce the oil price sensitivity by about at least 15% and the currency sensitivity by at least 25%. The proportion on non-South Africa earnings will rise, with the US potentially over 30%, South Africa at around 50% and with Europe, Middle east, Asia and Africa the balance.

Profitability beyond 2019/2020 seems encouraging from this vantage point.

Share price of Sasol in ZA cents