Take a listen to Mark's thoughts here.

Share price: R92,71

Net shares in issue: 320,8 million

Market cap: R29,7 billion

Exit PE ratio 19,6x; forward PE 18,4x

Dividend yield 4,0%

Fair value: R92

Target price: R100

Trading Buy and Portfolio Buy

Key takeaway:

AVI has reported annual earnings in line with my expectation. My earnings estimate has been maintained for some months at 463,4 cents per share, a rise of 10,4%, with earnings of R1 488 million estimated versus R1 339 million. In practice, EPS has come out at 464,1 cents, up 10,6%, with rand earnings at R1 492 million.

My three-year forecast CAGR on EPS remains at 10,2%.

Revenue for the year is up 8,4% to R12,2 billion compared with a rise of 6,5% to R6,4 billion at the interim stage. Operating profit margin is higher at 17,7% with the result that operating profits are up 12,4%.

The interim dividend was up 13,6% to 150 cents and the final dividend is 220 cents, slightly higher than my forecast of 217 cents, which therefore makes for an annual dividend of 370 cents.

Recommendation:

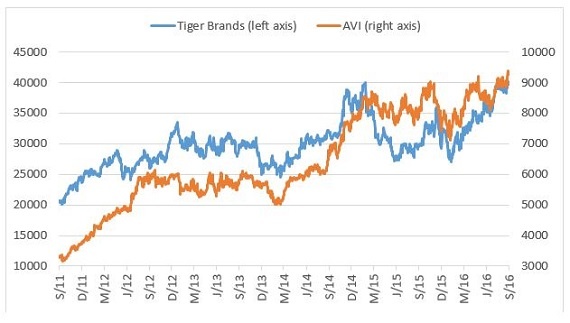

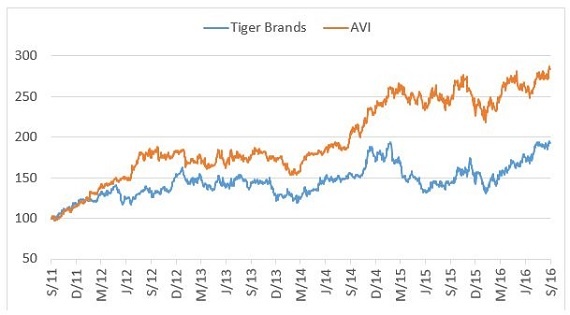

In a note called “Divergent paths” dated 28 July, I analysed AVI and Tiger Brands as comparative investments. The title pretty much sums up why AVI has been a preferred exposure. Tigers is now having to panel beat itself in to shape whilst AVI is a humming machine.

AVI is not cheap. The EV/EBITDA ratio exceeds 12x and the exit PE ratio is 19,6x. But the yield on an annual dividend of 370 cents is 4,0%, which is nice. AVI offers a substantially higher dividend yield due to the fact that the cash flow profile enables a far more generous dividend than Tiger Brands without compromising capital expenditure.

Trading Buy and Portfolio Buy maintained with a fair value maintained at R92 with the target price R100.

AVI and Tiger Brands based to 100

AVI and Tiger Brands share price in ZA cents