Suitability: Satrix Resi is a specialist fund that invests in companies in the resources sector, including mining and oil & gas companies. Its constituents, which are exposed to commodity prices, are likely to move in the same direction. While this is a plus during a commodity boom it often results in large losses during a downturn. Largely because of that, this ETF suits investors who can stomach return variability and already have a diversified portfolio (one which includes other equity holdings, cash and bonds). The investor should also be willing hold the shares through the cycle.

The resources sector has been through a rough time over the past few years as commodity prices have plummeted, but they have shown signs of life this year. Share prices for most mining companies have recouped some of the losses recorded in 2015. But despite the recovery most of the constituents of this ETF are still trading at a fraction of what their prices were just before the start of the collapse in commodity prices two years ago.

Click here for general information and benefits of ETFs. You can also read our other ETF Tuesday pieces here

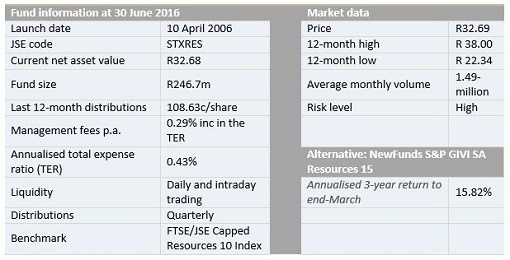

What it does: The ETF replicates the price performance of the FTSE/JSE Resources 10 index, which consists of the 10 largest companies ranked by full market value in the oil & gas and basic materials industries.

Disadvantages: One main flaw of this ETF is that it is weighted by market capitalisation (share price multiplied by number of shares in issue). Market-cap weighted indices tend to reflect historical performance. Although economic theory tells us that share prices are the present value of the sum of future expected returns, and therefore forward-looking, the market cap index is not based on expectations of future performance. Largely because of that we prefer the NewFunds S&P GIVI SA Resources 15 ETF, whose selection criteria are forward-looking with stock selection based on a company’s expected performance.

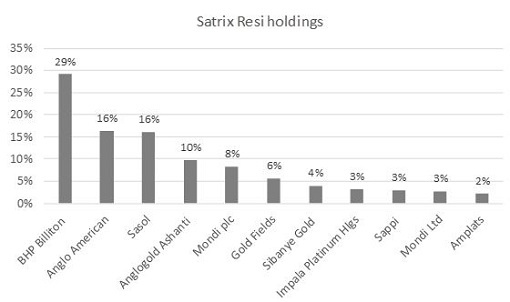

Top holdings: Eight of the fund’s constituents are mining companies with BHP accounting for 29% of the fund.

Risk: There are two important risks to consider. First, the fund is concentrated in one broad sector and all companies respond to similar risk factors. Furthermore, the large BHP holding accentuates the concentration risk. It is important therefore that this ETF forms part of a wider portfolio that includes other sectors. Second, it is an all-equity investment which is more volatile than other asset classes such as bonds and cash.

Fees: The ETF is relatively pricy compared to its closest alternative. It has an annualised total expense ratio of 0.43%.

Historical performance: The performance of an investment in an ETF depends on the method used to invest. A lump-sum investment will mimic the ETF performance exactly. However, investing through regular instalments will result in an annualised return in your portfolio which is different from that of ETF fund. The return in your portfolio will depend on the timing of your instalments.

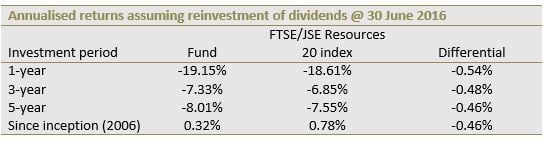

The returns in the table below are for a lump-sum investment. Satrix Resi has been going through some tough times lately. It has returned a mere 0.32% a year to those who invested at its inception in 2006.

Fundamental view:The Satrix Resi is trading at levels last seen in 2012. This is certainly an opportunity if you are bullish on commodity prices. The collapse in commodity prices, which started in mid-2014 when China slowed its consumption of industrial resources, decimated the fund. There has been an uptick in commodity prices this year and the weak rand has further boosted returns. This, however, does not mean that the commodity bear market is over – there is still far too much supply around relative to demand – but the bottom of the cycle may be in sight.

Most companies in the sector are undergoing dramatic restructurings that will leave them more efficient and potentially able to deliver serious value for shareholders should commodity prices rise. However, we expect most of the ETF’s constituents to cease or cut dividends until a meaningful recovery in commodity prices has been achieved.

Alternatives: Its closest peer is the NewFunds S&P GIVI SA Resources 15 which replicates the price performance of the S&P GIVI SA Resources Index, which represents the top 15 resource stocks from the S&P GIVI (Global Intrinsic Value Index) SA composite index of general equities. NewFunds S&P GIVI SA Resources 15 is much cheaper with an annual TER of 0.16%.

Other options are single-commodity ETFs. These invest directly in one commodity, bypassing the mining companies. For example, the Absa NewGold ETF invests in gold bullion debentures which are backed by physical gold. It is a way to invest in gold without having to invest in the mining companies that produce it. However, these are not allowed in tax-free savings accounts.

BACKGROUND: Exchange-traded funds (ETFs)

Exchange-traded funds (ETFs) are passively managed investment funds that track the performance of a basket of pre-determined assets (in this case, resource companies). They are traded the same way as shares and the main difference is that whereas one share gives exposure to one company, an ETF gives exposure to numerous companies in a single transaction. ETFs can be traded through your broker in the same way as shares, say, on the EasyEquities platform. In addition, they qualify for the tax-free savings account, where both capital and income gains accumulate tax free.

Benefits of ETFs

- Gain instant exposure to various underlying shares in one transaction

- They diversify risk because a single ETF holds various shares

- They are cost-effective

- They are liquid – it is usually easy to find a buyer or seller and they trade just like shares

- High transparency through daily published index constituents

Disclaimer

This research report was issued by Intellidex (Pty) Ltd. Intellidex aims to deliver impartial and objective assessments of securities, companies or other subjects. This document is issued for information purposes only and is not an offer to purchase or sell investments or related financial instruments. Individuals should undertake their own analysis and/or seek professional advice based on their specific needs before purchasing or selling investments. The information contained in this report is based on sources that Intellidex believes to be reliable, but Intellidex makes no representations or warranties regarding the completeness, accuracy or reliability of any information, facts, estimates, forecasts or opinions contained in this document. The information, opinions, estimates, assumptions, target prices and forecasts could change at any time without prior notice. Intellidex is under no obligation to inform any recipient of this document of any such changes. Intellidex, its directors, officers, staff, agents or associates shall have no liability for any loss or damage of any nature arising from the use of this document.

Remuneration

The opinions or recommendations contained in this report represent the true views of the analyst(s) responsible for preparing the report. The analyst’s remuneration is not affected by the opinions or recommendations contained in this report, although his/her remuneration may be affected by the overall quality of their research, feedback from clients and the financial performance of Intellidex (Pty) Ltd.

Intellidex staff may hold positions in financial instruments or derivatives thereof which are discussed in this document. Trades by staff are subject to Intellidex’s code of conduct which can be obtained by emailing mail@intellidex.coza.

Intellidex may also have, or be seeking to have, a consulting or other professional relationship with the companies mentioned in this report.