2016 was a bad year for ETF investors as all the major indices failed to produce decent returns. The top 40, one the most popular indices on the JSE, ended the year 1.83% lower than it was at the beginning of the year. The all share index, which includes all listed stocks, delivered a measly 2.4% return. Even the offshore ETFs, which have traditionally been regarded as safe havens in uncertain times, disappointed as they all registered negative growth.

This performance came on the back of a year characterised by a low-growth macroeconomic environment and market uncertainty spurred by the volatile domestic political situation, concerns over the direction of governance and economic policy in general – as well as the risk of a downgrade in South Africa’s credit rating. The heightened geopolitical uncertainty in the US, Europe and Middle East as well as slowing economic growth in China also contributed to the subdued performance.

Most of these risks are still present and are likely to continue supressing much-needed private sector investment and economic growth. Despite avoiding a cut to junk status in 2016, a credit ratings downgrade is still possible.

National Treasury expects economic growth to come at 1.3% in 2017. While this would be an improvement on 2016’s growth, estimated to be 0.5%, we don’t think it will be sufficient to bolster investor confidence.

Political developments within the ANC, which is scheduled to elect its new leadership at its elective conference in December, are also likely to be key to prospects. Given this background we can’t rule out political shocks during the year. There are some who still believe President Jacob Zuma might reshuffle his Cabinet, possibly removing Pravin Gordhan as finance minister.

The best performing index tracker funds last year were not ones that focused on market capitalisation and high liquidity, but Smart Beta ETFs which use other risk factors such as

value, dividends, volatility and fundamental indexation to search for pockets of value.

Are we going to see the same trend this year? Below are Intellidex’s picks in each of the five broad categories of investment strategies. Not all categories are appropriate for all investors – it depends on your personal circumstances – but the funds we pick are the ones we think are most appropriate in each category.

Local equities

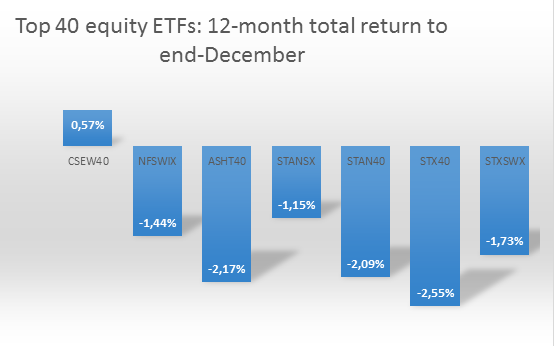

There are a range of funds which invest in local equities but we prefer those that track the performance of the top 40 index. The key attraction with the top 40 funds is their ability to provide diversification and stable returns over the long term, which is desirable in uncertain times.

We prefer those which track using the Swix weighting method rather than the traditional JSE top 40 index which is determined by market capitalisation. The Swix weights constituents based on the share capital held in electronic records and registered in the SA share register. It therefore excludes shares held outside SA and this results in reduced exposure to cyclical commodities, which improves diversification and stability of returns.

We like any of the three Swix-weighted top 40 funds (Satrix Swix, NewFunds Swix 40 or Stanlib Swix) but we pick the Stanlib Swix 40 because of its lower expense ratio. While the CoreShares Equally Weighted Top 40 was the best performer in 2016 its long-term historical performance is not as impressive. Its one drawback is that it is likely to miss out on any sustained run in the share price of a company because its allocation will always be limited to 2.5%.

Foreign equities

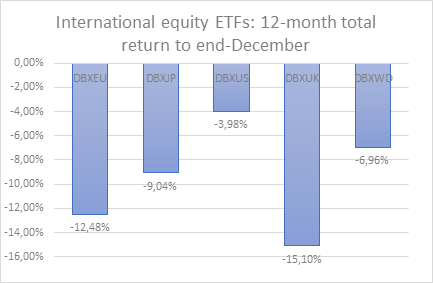

The international ETFs are proving to be quite a hit among local investors, spurred partly by localy political turbulence and an uninspiring growth trajectory. It’s quite common for investors to seek growth elsewhere if they feel their local markets are unlikely to yield meaningful growth.

Last year we chose db x-tracker USA as our pick in this category. The fund went on to outperform its peers. While we still prefer the US fund over its its peers – Japan, UK and the eurozone – we change our pick in this category to CoreShares S&P 500.

While it’s still new with no historical record, we are attracted by its total expense ratio (TER) which is expected to be between 0.55% and 0.65%. That will be way cheaper than the db x-trackers with an average TER of 0.8%. Given that the two track indices with a similar return profile – the S&P 500 and MSCI US – we think CoreShares’ lower cost structure will likely help it outperform its peers.

Property ETFs

There are a few property-focused ETFs to choose from but our choice is the CoreShares PropTrax 10, which uses an equally weighted index that reduces the idiosyncratic risk of individual companies. Property has been a bright part of the JSE over the past few years but Brexit developments created uncertain prospects for companies with UK exposure.

There are a few property-focused ETFs to choose from but our choice is the CoreShares PropTrax 10, which uses an equally weighted index that reduces the idiosyncratic risk of individual companies. Property has been a bright part of the JSE over the past few years but Brexit developments created uncertain prospects for companies with UK exposure.

The CoreShares PropTrax 10 ETF has maintained its top performance within the segment, returning 10.42% in 2016.

Bond and cash funds

Bond and cash funds

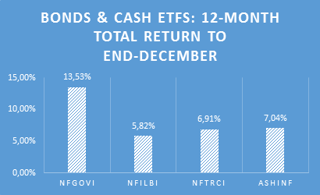

All the funds described ab ove are predominantly equity investments. However, bonds and cash have distinct risk properties which, when combined with equity investments, produce better risk-adjusted returns. There are four listed funds in this category:

ove are predominantly equity investments. However, bonds and cash have distinct risk properties which, when combined with equity investments, produce better risk-adjusted returns. There are four listed funds in this category:

(i) NewFunds GOVI ETF;

(ii) NewFunds ILBI ETF;

(iii) NewFunds TRACI 3 Month ETF;

(iv) Ashburton Government Inflation ETF.

They each track different things: (i) tracks government bonds; (ii) & (iv) track inflation-linked government bonds; and (iii) tracks short-term money market instruments.

If you are investing for a very short period, usually less than a year, then we prefer the NewFunds TRACI 3 Month as it is the least sensitive to sudden adverse interest rate movements. This is as close to cash as you can get.

For a longer investment horizon, our preference is guided by caution, particularly in emerging markets where various external and internal variables can drive up the inflation level. So we would choose an inflation-linked bond to cushion investors from unseen inflation pressures. Because the NewFunds ILBI ETF has a lower expense ratio, it is our choice here.

Dividend-focused funds

We believe returns should be considered on a total return basis rather than just looking at the income (dividend) return component.

Whereas the Satrix Divi pools its assets from the top 40 index, the Coreshares Dividend Aristocrat ETF extends its pool to mid-caps. We prefer the Satrix Divi because it is forward-looking, based on projected dividends. The CoreShares fund is based on historical performance that may not be repeated in future.

Whereas the Satrix Divi pools its assets from the top 40 index, the Coreshares Dividend Aristocrat ETF extends its pool to mid-caps. We prefer the Satrix Divi because it is forward-looking, based on projected dividends. The CoreShares fund is based on historical performance that may not be repeated in future.

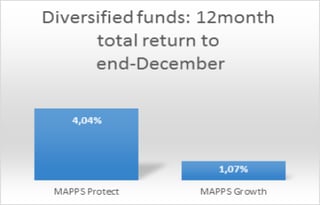

Diversified funds

Equities are regarded as the financial asset class that carries the most risk. They generally provide the best returns over time, which compensates for the high short-term risk, so they are more suited to longer-term investors.

One way to reduce that risk is to invest in funds that include other asset classes such as bonds and cash. Two good funds for this are the NewFunds MAPPS Protect ETF and the NewFunds MAPPS Growth ETF.

One way to reduce that risk is to invest in funds that include other asset classes such as bonds and cash. Two good funds for this are the NewFunds MAPPS Protect ETF and the NewFunds MAPPS Growth ETF.

They are designed to meet two different risk appetites: Protect is suitable for older savers nearing retirement and Growth is for younger savers with a longer time horizon.

Disclaimer

This research report was issued by Intellidex (Pty) Ltd. Intellidex aims to deliver impartial and objective assessments of securities, companies or other subjects. This document is issued for information purposes only and is not an offer to purchase or sell investments or related financial instruments. Individuals should undertake their own analysis and/or seek professional advice based on their specific needs before purchasing or selling investments. The information contained in this report is based on sources that Intellidex believes to be reliable, but Intellidex makes no representations or warranties regarding the completeness, accuracy or reliability of any information, facts, estimates, forecasts or opinions contained in this document. The information, opinions, estimates, assumptions, target prices and forecasts could change at any time without prior notice. Intellidex is under no obligation to inform any recipient of this document of any such changes. Intellidex, its directors, officers, staff, agents or associates shall have no liability for any loss or damage of any nature arising from the use of this document.

Remuneration

The opinions or recommendations contained in this report represent the true views of the analyst(s) responsible for preparing the report. The analyst’s remuneration is not affected by the opinions or recommendations contained in this report, although his/her remuneration may be affected by the overall quality of their research, feedback from clients and the financial performance of Intellidex (Pty) Ltd.

Intellidex staff may hold positions in financial instruments or derivatives thereof which are discussed in this document. Trades by staff are subject to Intellidex’s code of conduct which can be obtained by emailing mail@intellidex.coza.

Intellidex may also have, or be seeking to have, a consulting or other professional relationship with the companies mentioned in this report.