In the final local ETF monthly review of the year by Intellidex, the research team highlights market events, the domestic economic outlook, and, of course, their favoured Exchange Traded Funds. Why else would we be here?

Locally, resource counters drove the all share index, with the gold and platinum indices climbing 22% and 16.7% respectively in October.

The Macroeconomic view

Both the medium-term budget statement and the Eskom policy paper were disappointing, but the bourse got a boost from mining heavyweights. There was some relief for SA as Moody’s retained its investment grade status – the only international credit rating agency that has not junked SA’s sovereign credit rating. However, Moody’s did downgrade the country’s outlook to negative from stable.

Our country is at a critical point with failing government finances and limited political will/power to implement much-needed reforms. This is being felt on the JSE which has remained largely flat over the past five years, in contrast to high-performing offshore equities. The underwhelming medium-term budget and Eskom policy paper were followed by the downgrading of our outlook to negative from stable by Moody’s, although we maintained our sovereign credit rating at investment grade.

Government’s debt metrics have deteriorated faster than projected at the beginning of the year. While retaining Moody’s investment grade buys us a few months to sort out the mess, it’s difficult to see government taking drastic measures given that it has failed to act decisively since 2018.

While some SA assets enjoyed a bounce because we were not junked straight away, it may just be a precursor to an inevitable downgrade. The risk of being junked after the 2020 budget in February has increased substantially.

Due to a lack of policy cohesion within the ruling ANC, President Cyril Ramaphosa failed to ride the positive wave of sentiment following his ascendancy to the helm of both the ANC and the country at the end of 2017.

Compared with the strong sentiment that characterised the beginning of 2018, the consumer confidence gauge has since fallen back to levels last seen in the Zuma era. National Treasury has slashed its 2019 GDP growth forecast to 0.5% from 1.5% and unemployment is at its highest level in more than a decade. We believe nothing short of action in reform implementation will cut it, otherwise a downgrade seems inevitable.

In this context, we think SA-facing stocks, even at these low valuations which are somewhat justified by broad-based poor earnings, will remain unloved in the foreseeable future – as will government debt. However, the all share index will likely get support from the big mining counters and companies that generate the bulk of their earnings outside SA, as the rand is set to remain on a losing streak.

ETFs featured

Local:

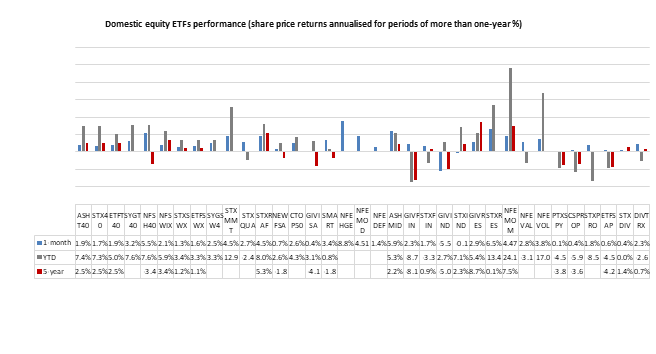

With the local economy facing numerous challenges, robust risk management practices should be employed in portfolios. While we feel the Satrix SA Quality fund implicitly achieves this through its multi-dimensional approach to the selection of its constituents, there is a new (re-branded) multi-factor ETF which explicitly takes volatility into account as one of six factors it employs in fund construction.

The CoreShares Scientific Beta Multifactor Index ETF fits our mould of a good investment philosophy as it is built with risk factors in mind. It was launched in May and has a great back-tested track record. We maintain our choice for local broad-based equity exposure with this new multifactor fund. The fund was up 3.4% in October.

There are extensions to this core local equity exposure that can be added in a tactical sense as a satellite fund. The NewFunds Equity Momentum fund (up 4.5% in October) is worth considering. It has performed far ahead of other equity funds under all market extremes in the past five months and has a year-to-date return of 18.8%.

Click logo to view ETF

Commodities:

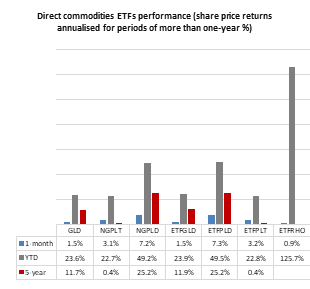

Adding a commodity ETF to your portfolio improves diversification because commodities march to the beat of their own drum – they are not in sync with broader markets. Traditionally, gold is the preferred addition to an investor’s portfolio because over longer periods it has shown to be the least correlated with other assets. However, our preference based on our medium-term outlook is between rhodium and palladium.

The new vehicle emission laws in Europe and China are driving demand for both commodities and this is expected to continue in the foreseeable future. We are slightly more inclined towards rhodium because it is scarcer, with lower extraction rates from PGM ore. The primary production of rhodium is somewhat inelastic and is expected to decline moderate moderately over the medium term. Palladium funds gained northwards of 7.0% during October.

Important note: These ETFs do not qualify for a tax-free savings account.

Click logos to view ETF

There's plenty more from where that came from. The team at Intellidex have more insights for the month of November. To see more in-depth analysis and market insights (global and local), check out the full note here.

Background: Exchange-traded funds (ETFs)

Exchange-traded funds (ETFs) are passively managed investment funds that track the performance of a basket of pre-determined assets. They are traded the same way as shares and the main difference is that whereas one share gives exposure to one company, an ETF gives exposure to numerous companies in a single transaction. ETFs can be traded through your broker in the same way as shares, say, on the EasyEquities platform. In addition, they qualify for the tax-free savings account, where both capital and income gains accumulate tax free.

Benefits of ETFs

- Gain instant exposure to various underlying shares or bonds in one transaction

- They diversify risk because a single ETF holds various shares

- They are cost-effective

- They are liquid – it is usually easy to find a buyer or seller and they trade just like shares

- High transparency through daily published index constituents

If you thought this blog was interesting, you should also read:

Disclaimer

This research report was issued by Intellidex (Pty) Ltd. Intellidex aims to deliver impartial and objective assessments of securities, companies or other subjects. This document is issued for information purposes only and is not an offer to purchase or sell investments or related financial instruments. Individuals should undertake their own analysis and/or seek professional advice based on their specific needs before purchasing or selling investments. The information contained in this report is based on sources that Intellidex believes to be reliable, but Intellidex makes no representations or warranties regarding the completeness, accuracy or reliability of any information, facts, estimates, forecasts or opinions contained in this document. The information, opinions, estimates, assumptions, target prices and forecasts could change at any time without prior notice. Intellidex is under no obligation to inform any recipient of this document of any such changes. Intellidex, its directors, officers, staff, agents or associates shall have no liability for any loss or damage of any nature arising from the use of this document.

Remuneration

The opinions or recommendations contained in this report represent the true views of the analyst(s) responsible for preparing the report. The analyst’s remuneration is not affected by the opinions or recommendations contained in this report, although his/her remuneration may be affected by the overall quality of their research, feedback from clients and the financial performance of Intellidex (Pty) Ltd.

Intellidex staff may hold positions in financial instruments or derivatives thereof which are discussed in this document. Trades by staff are subject to Intellidex’s code of conduct which can be obtained by emailing mail@intellidex.coza.

Intellidex may also have, or be seeking to have, a consulting or other professional relationship with the companies mentioned in this report.