ETF ANALYSIS

Performance review

This ETF follows smart beta construction criteria, using alternative index construction rules instead of the typical cap-weighted index strategy. It takes into account factors such as size, value and volatility – and its 2016 performance is quite telling. It performed significantly poorer than the all share index over the past five years. NewFunds compares the fund’s performance with the all share index and although this contravenes the principles of benchmark tracking, it shows how smart beta can significantly diverge from a pure indexing strategy.

In the year to end-December the fund lost 9.25% compared with a 2.63% gain on the overall market.

Outlook: This fund constitutes blue-chip stocks with international operations and multi-currency income streams. So the value of the fund is driven by economic developments both locally and abroad, including exchange rate movements.

While most economic growth forecasts for this year are around 1%, there are some promising signs. The inflation outlook appears favourable, which bodes well for consumer demand. This is augmented by a good 2016/17 rain season; stable and improving commodity prices; a strengthening rand; and a softening global interest rate path. Furthermore, growth in other countries – where some of the fund’s constituent companies operate – is better than in SA, although the rand’s recent strength is likely to neutralise translated foreign earnings.

Additionally, investors should note that although equities are one of the most volatile asset classes, this fund is constructed to minimise volatility.

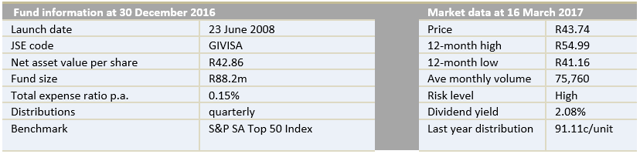

Key facts:

Suitability

The fund is ideal for investors with a medium- to long-term investment horizon and can be used as part of a core investment portfolio. Equity investments tend to exhibit higher short-term volatility than other asset classes, so a longer investment horizon gives a portfolio time for returns to overcome volatility and accumulate gains.

What it does

Since its inception until June 2015, this ETF tracked the eRAFI Overall SA Index which was made up of the top 40 SA companies ranked by fundamental valuation metrics. After the eRAFI was discontinued, the fund started tracking the S&P GIVI SA Top 50, which represents the top 50 stocks from the S&P GIVI (Global Intrinsic Value Index) SA composite index of general equities. The smart beta approach it uses selects stocks assessed to have the highest intrinsic value and lowest volatility, subject to certain liquidity constraints. The intrinsic value of each stock is determined by its book value and its discounted projected earnings.

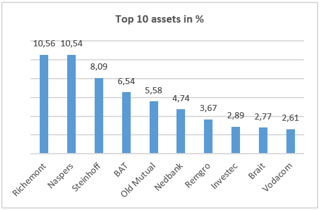

Top holdings: The top 10 holdings of this ETF make up 58% of the fund. The fund is dominated by financials and consumer goods and services

Top holdings: The top 10 holdings of this ETF make up 58% of the fund. The fund is dominated by financials and consumer goods and services

Risk: Although the stock and sector diversity in the portfolio reduce the investment risk over the medium to long term, the ETF is still based on securities with inherent trading risks. The value of the investments will therefore rise and fall as markets fluctuate. Your capital is not protected.

Alternatives

The CoreShares Top 50 ETF, launched in 2015, tracks the same index as NewFunds S&P GIVI Top 50 so it also follows a smart beta approach. However, CoreShares Top 50 has a higher total expense ratio of 0.32%.

Benefits of ETFs

- Gain instant exposure to various underlying shares or bonds in one transaction

- They diversify risk because a single ETF holds various shares

- They are cost-effective

- They are liquid – it is usually easy to find a buyer or seller and they trade just like shares

- High transparency through daily published index constituents

|