ETF ANALYSIS

Performance review

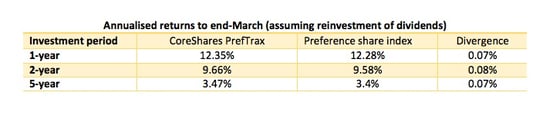

Preference shares listed on the JSE have enjoyed a solid performance over the past two years. The preference shares index returned 9.58% a year in the two years to end-March, outperforming both the JSE all bond index (5.04%/year) and the JSE Top 40 index (2.64%/year). Benefiting from this, the CoreShares PrefTrax ETF returned 12.35% over the 12 months to end-March and 9.7% over a two-year period.

The strong performance by bonds and preference shares may be attributed to the rising economic uncertainty on the investment markets. In such times, investors tend to shift their portfolios towards less riskier assets, usually fixed income assets.

Outlook

While preference shares have performed well over the past two years, they have been a largely disappointing asset class for investors over the long term. CoreShares PrefTrax has returned 3.5%/year over the past five years – way below inflation, which averaged about 6.3% over that period.

A preference share is a hybrid between normal shares and debt. That has implications for the way they are taxed and for the riskiness of the investment. Preference shares come with a right to receive a set dividend, but companies can pass this dividend if they are unable to pay it, in which case it either accumulates to the next period or the obligation falls away – the difference depends on exactly what kind of preference share is involved. Because these payments are technically dividends, they are taxed as dividends rather than interest, which is taxed at income tax rates for amounts above a certain threshold. The increase of the dividend tax in the February budget from 15% to 20% is therefore a direct hit on the returns that preference share investors can expect. Preference shares are also higher risk than normal debt instruments because the company has that right to pass the dividend. Also, if the company goes bankrupt, preference shareholders rank behind lenders and other creditors. That is a real risk, and was made clear in the collapse of African Bank when preference shareholders lost a considerable portion of their investment.

The returns earned consist of the dividend flows plus any movement in the price of the preference shares. Most preference shares pay a dividend as a function of the prime interest rate, so the notional price of the preference share moves little, usually reflecting the financial health of the company and its ability to meet the preference dividend obligation.

In the long run, expectations on interest rates cycles have a bigger say on the performance of preference shares. If the market expects the prime interest rate to increase, demand for preference shares increases as investors seek higher preference share yields that are linked to prime, as opposed to equity. This should, however, be analysed in the context that investors don’t only compare preference shares to ordinary shares but also to interest-bearing assets. Investors often weigh up whether they can generate superior returns in interest-bearing accounts (money-market accounts and bonds) or through preference shares. When interest-bearing instruments are expected to provide higher yields, investors will move away from preference shares.

Effectively what preference share investors would like to see is a higher prime rate and a widening of the gap between preference share yields and other income alternatives. A higher interest rate looks likely given the recent downgrades to SA’s credit rating. However, it’s difficult to say what effect this will have on the spread between the preference shares yield and that of bonds. The tax factor, discussed below, is also an important issue to consider.

Suitability

CoreShares PrefTrax shares is likely to appeal mainly to high net worth, income-focused investors. In SA, a dividend withholding tax of 20% is paid on dividends earned from preference shares, giving them a tax advantage over bonds and money market instruments which are taxed at the marginal income tax rate of the taxpayer once the interest exemption of R23,800 is used up. Share capital appreciation is limited, so when investing in this ETF your main aim should be to generate income over a long period.

What it does:

CoreShares PrefTrax tracks the FTSE/JSE preference share index in the same weightings in which they are included in the index. The JSE preference share index measures the performance of non-convertible, floating rate perpetual preference shares (these are the most standard form of preference share which cannot be converted to ordinary equity, or recalled by the company).

Weakness

The preference share market is less liquid than the market for ordinary shares, making the fund more susceptible to short-term capital fluctuations because of changes in investor sentiment towards the asset class.

Top holdings

Close to three quarters of the fund’s assets are invested in preference shares issued by banks. Standard Bank tops the list with 18%, followed by Absa, FirstRand and Nedbank, each of which contributes at least 13%. Investments in preference shares issued by non-financial counters account for less than 10% of the fund.

Fees

Total expenses take 0.57% from the fund each year.

Alternatives

Investors do not have many options when it comes to ETFs which track preference shares. Some of the attributes of preference shares, however, can be found through bond ETFs. We list available bond ETFs below. The main weakness with the bond ETFs (except the Asburton Inflation-X ETF) is that they are total return ETFs. This means that as these funds receive periodic interest payments from their underlying investments, they do not distribute it to unit holders but issue more units.

Absa’s NewFunds Govi ETF tracks the performance of the SA government bond total return index (Govi).

NewFunds ILBI ETF, also issued by Absa, tracks the Barclays Capital/Absa Capital South African government inflation-linked bond total return index of eight RSA inflation-linked bonds.

The Satrix Ilbi is a more recent addition to the bond sector. It tracks the performance of the S&P South Africa Sovereign Inflation-Linked Bond 1+ Year Index.

If you enjoyed this blog, check out:

Benefits of ETFs

- Gain instant exposure to various underlying shares or bonds in one transaction

- They diversify risk because a single ETF holds various shares

- They are cost-effective

- They are liquid – it is usually easy to find a buyer or seller and they trade just like shares

- High transparency through daily published index constituents

|