The NewFunds Swix 40 and other funds that track SA’s major equity indices have been under pressure over the past three years. This is largely because waning investor confidence caused by rising economic and political uncertainty has seen equites underperforming bonds and cash.

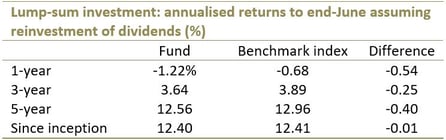

The NewFunds Swix 40 ETF shed 1.22% of its value in the 12 months to end-June on the back of mixed performances from its top holdings. Of its top 10 holdings, Anglo American, Standard Bank and Naspers were the biggest gainers, surging 35%, 17% and 15% respectively. Steinhoff, MTN and Remgro were the biggest losers, shedding 21%, 20% and 14% respectively.

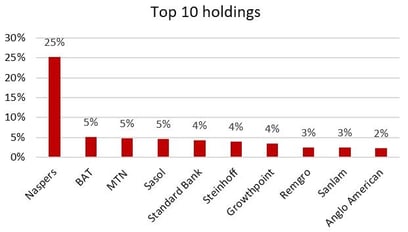

A major event was the delisting of SABMiller in the second half of last year following the acquisition of its shares by AB InBev. The delisting saw Naspers’ weighting in the fund increase to over 25%, more than double the size of the next two largest companies combined – BAT and MTN. Prior to that, Naspers accounted for 21% of the fund. While being disproportionately overweight in Naspers has been positive for the fund’s performance over the past few years, it has increased concentration risk. The danger of being so overweight in one stock is that if it goes down, it drags the entire fund with it.

What it does

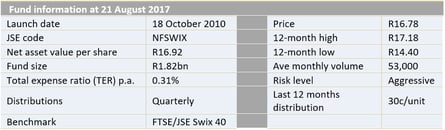

The NewFunds SWIX 40 ETF tracks the FTSE/JSE Shareholder Weighted (Swix) Top 40 Total Return Index. By considering the JSE register only, it means dual-listed stocks are down-weighted because a significant portion of their shares are held offshore. The ETF is therefore more representative of the universe of shares available to South African investors.

Performance review

The NewFunds ILBI ETF poorly in the 12 months to end-June, losing 0.8%.

Outlook

SA is officially in a technical recession, having recorded two consecutive quarters of negative GDP growth. On the political front, the fight for the ANC presidency is heating up and promises to be a dirty one. We believe these issues will continue fuelling uncertainty in the short term and while we expect some stock market volatility, we don’t see significant upside potential. However, the performance of this fund should be cushioned by significant holdings in more defensive, less volatile counters and exposure to companies that derive most of their revenue abroad.

Key facts

Suitability

The NewFunds Swix 40 ETF is ideal for investors with a medium- to long-term investment horizon. This fund invests in the 40 largest blue-chip companies on the JSE. Equity investments tend to exhibit higher short-term volatility than other asset classes, so a longer investment horizon gives a portfolio time for returns to accumulate ahead of volatility.

Top holdings

The top 10 stocks account for 56% of the fund, which we think is not bad from a diversification point of view. However, Naspers is the biggest investment with 25% of the fund in its shares, followed by British American Tobacco with 5%. Diversification across industries is also poor: two thirds of the fund are in two sectors: consumer related companies (43%) and financials (23%). The basic materials sector has the next biggest exposure with 9%, with four other sectors having less than 5% each.

Risks:

The fund is disproportionately overweight in Naspers, and is exposed to just a few sectors, reducing diversification benefits. Furthermore, this is a 100% investment in equities, which is a riskier asset class than bonds or cash. However, the returns over time should compensate for volatility. The constituent companies themselves do bring some other diversification benefits because they operate in several jurisdictions and varied sectors, which diminishes risk to a degree..

Fees

The NewFunds Swix 40 fund has a total expense ratio (TER) of 0.31%.

Alternatives

Alternative funds are the Satrix Swix 40 and Stanlib Swix 40 which both similarly track the Swix index.

Background: Exchange-traded funds (ETFs)

Exchange-traded funds (ETFs) are passively managed investment funds that track the performance of a basket of pre-determined assets. They are traded the same way as shares and the main difference is that whereas one share gives exposure to one company, an ETF gives exposure to numerous companies in a single transaction. ETFs can be traded through your broker in the same way as shares, say, on the EasyEquities platform. In addition, they qualify for the tax-free savings account, where both capital and income gains accumulate tax free.

Benefits of ETFs

- Gain instant exposure to various underlying shares or bonds in one transaction

- They diversify risk because a single ETF holds various shares

- They are cost-effective

- They are liquid – it is usually easy to find a buyer or seller and they trade just like shares

- High transparency through daily published index constituents

If you thought this blog was interesting, you should also read:

Disclaimer

This research report was issued by Intellidex (Pty) Ltd. Intellidex aims to deliver impartial and objective assessments of securities, companies or other subjects. This document is issued for information purposes only and is not an offer to purchase or sell investments or related financial instruments. Individuals should undertake their own analysis and/or seek professional advice based on their specific needs before purchasing or selling investments. The information contained in this report is based on sources that Intellidex believes to be reliable, but Intellidex makes no representations or warranties regarding the completeness, accuracy or reliability of any information, facts, estimates, forecasts or opinions contained in this document. The information, opinions, estimates, assumptions, target prices and forecasts could change at any time without prior notice. Intellidex is under no obligation to inform any recipient of this document of any such changes. Intellidex, its directors, officers, staff, agents or associates shall have no liability for any loss or damage of any nature arising from the use of this document.

Remuneration

The opinions or recommendations contained in this report represent the true views of the analyst(s) responsible for preparing the report. The analyst’s remuneration is not affected by the opinions or recommendations contained in this report, although his/her remuneration may be affected by the overall quality of their research, feedback from clients and the financial performance of Intellidex (Pty) Ltd.

Intellidex staff may hold positions in financial instruments or derivatives thereof which are discussed in this document. Trades by staff are subject to Intellidex’s code of conduct which can be obtained by emailing mail@intellidex.coza.

Intellidex may also have, or be seeking to have, a consulting or other professional relationship with the companies mentioned in this report.