![]()

This week, the following key stocks will be topical – Discovery, Sanlam and Steinhoff. With a collective market capitalisation of R530 billion these are top companies in their own right regardless of the JSE index weighting. Here’s what you need to know in advance.

Life Insurance

Share price: R123.75

Net shares in issue: 644,2 million

Market cap: R79,7 billion

Embedded value per share estimate: R92,11; return on EV 16%

Exit PE ratio 17,4x; forward yield 1,7%; price to EV 1,34x

Fair value: R120

Target price: R130

Trading Sell and Portfolio Buy

Health and life insurer Discovery reports full year results on Tuesday. What to look for?

Normalised earnings per share will be around 682 cents. Whilst earning per share will be up a modest 2% this is due in part to the effect that the rights issue last year has on the denominator. Earnings in rand should be up about 8% to R4 350 million whilst profit from operations is likely to come in at just under R6 500 million, up 12%.

Discovery had an underwritten renounceable R5 billion rights issue with effect from 7 April 2015 that resulted in shares in issue increasing by 55,6 million shares to 647,4 million shares (up 9%), excluding treasury shares. The purpose, inter alia, was for growth in Vitality Life and DiscoveryCard.

Whilst investment in growth and new lines of business has a depressive effect on earnings in the short term, underlying profitability remains robust and the strategy clearly defined. Potential regulatory risks around healthcare are a limiting factor for the time but I don’t see this as a reason to avoid the stock.

The interim dividend in rand was up 10% but due to the extra shares in issue the dividend in cents was flat at 85,5 cents. I estimate a final dividend of 91 cents, which would bring the potential annual dividend to 176,5 cents and compares with 174,5 cents last year.

In my model, I have estimated embedded value per share as at 30 June 2016 to be 9211 cents, growth of 11% on the reported 8314 cents as at June 2015 and up 5% compared with the 8740 cents as at December 2015. Embedded value in rand is estimated to be R59,3 billion, up 13% compared with June 2015.

From an actuarial point of view, the concept of embedded value is key to understanding how underlying present value of business on the books is derived. Typically, embed value is higher than net asset value, an accounting calculation. My NAV estimate is R33 billion so EV is 80% more than NAV.

Discovery attracts a premium rating, probably for good reason. The current share price of R123,74 is a 34% premium to EV. A year ago, the premium was 62%.

Sanlam, at R64,39 per share, trades at a 25% premium to EV.

MMI, at a share price of R23, trades at an 8% discount to EV and typically does so.

However, the divergence in valuation metrics does not necessarily make Discovery or Sanlam a poor buy in relation to MMI.

Discovery remains on a growth trajectory although a weak rand does inhibit purchasing power of investment offshore.

Recent initiatives include the Bankmed medical scheme administration and managed care contract, expansion of the business model into banking, the Chinese business Ping An Health and development of VitalityHealth in the UK.

Ping An Health in China is playing its part to grow the health insurance industry in China. New business is growing exponentially with new annualised premium income likely to be 80% higher for the year and exceeding 9% of group API compared with 6% last year.

Ping An and other developmental assets are currently detracting from earnings to the extent of approximately R500 million.

Discovery is on a rolling exit price earnings multiple of 17,4x and a forward price earnings ratio of 15,5x based on my current (unchanged) estimates. The Bloomberg PE of 22x is correct based on the run rate of reported earnings but makes no adjustments for either non-cash or non-operational debits and credits to P&L.

I’ve maintained a cautious stance on all interest rate sensitive stocks, not least because of unpredictable political risks and the impact that has on bond pricing and thus present values of stocks. I’d not be chasing any of the insurers, including Discovery.

As a growth stock, Discovery pays out much less in dividends than peers. The company has an annual cover ratio of 3,9x. The gross yield is currently 1,4%.

I have maintained a fair value of up to R120, which allows for rises in interest rates, with the target price at R130.

Let’s see what happens with the results but meantime the call is Trading Sell and Portfolio Buy.

Life Insurance

![]()

Share price: R64,39

Net shares in issue: 2 003 million

Market cap: R129 billion

Embedded value: R51,63; return on EV 13%

Exit PE ratio 14,4x; forward yield 4,0%; price to EV 1,25x

Fair value: R62

Target price: R67

Trading Sell and Portfolio Buy

The days of Crimplene safari suits are a distant memory and an Irish chartered accountant now calls the shots in the C-suite. A Bellville head office has been no hindrance to progress either. Sanlam is a well-run business from which Old Mutual could take some strategic lessons. Its green coloured competitor, which remains a strong rival on the home front, has learned expensively how not to keep up with the Jonses and is preparing to decamp from Lambeth Hill, London.

Sanlam has been diversifying across geography, segments and product. For example, Saham Finances, 30% of which was acquired for $375 million, has contributed to earnings with effect from 1 March 2016.

From an income yield point of view, Sanlam is both secure and attractive. Earnings growth in the prevailing economic situation though will be difficult to achieve but the quality of earnings is undoubted.

For the year ending December 2015 Sanlam grew adjusted earnings by 6% but it was a mixed outcome and overall slightly better in the second half versus the first half. I expect a tepid result when Sanlam reports earnings for the six months to 30 June on Thursday.

Investment returns ups and downs on the capital portfolio are impossible to forecast with any accuracy and affected by factors largely beyond management control, including the exchange rate.

My current estimate is for normalised growth of 4,9% in F2016 and my three-year compound growth estimate is 8%.

Capital adequacy is not an issue with life insurance having a more than 5x cover ratio – among the best in the industry (Discovery is on 4x).

Sanlam Personal Finance is showing growth with a change in mix away from individual life. The Glacier platform is benefitting from demand for the offshore and wrap products.

Emerging Markets is achieving double digit growth in new business.

Sanlam Investments is likely to have shown around 5% growth in new business volumes, assisted by Employee Benefits and International. However, recurring premium risk business is weak.

Investment Management, 12% of profits, can be expected to deliver flat numbers on weaker fee income. PIC funds were lost in 2014 and 2015, skewing the base slightly.

Santam, in which Sanlam has a 61,6% holding, has already reported and returned strong underwriting results for the six months with maintained growth of 8% in gross written premiums. Santam’s solvency ratio of 51% is higher than the target range of 35% to 45% of net written premiums. The economic capital coverage ratio of 178% is ahead of the target of 130% to 170%.

Santam declared a special dividend of 800 cents per share or R920 million so Sanlam’s attributable share is R567 million. The gross interim ordinary dividend declared was 311 cents per share, up 8%. This is R357 million, of which Sanlam has an attributable share of R220 million.

Business outside South Africa is still small but growing. Around 89% of the value of new business together with the same proportion of profit is South Africa and neighbouring territories with 7% other Africa and 4% elsewhere. It is feasible for non-South Africa business to increase to 20% within the foreseeable future.

Investors should recall that Sanlam is a traditional insurer with life and general insurance 76% of profits - with life 62% alone. Discovery’s life business by contrast is 47% of group profits, before development losses, followed by health at 32%.

Return on embedded value at approximately 13% compares favourably with Discovery on 16% given the mix differences.

Sanlam declares one annual dividend so there will be no interim declaration.

Although not to the same degree as banks, the stock is sensitive to movements in bond yields.

Despite having retreated from levels close to R70, at R64 Sanlam remains, from a relative point of view, in my Trading Sell category. It remains a Portfolio Buy. Fair value is R62 and the target price R67.

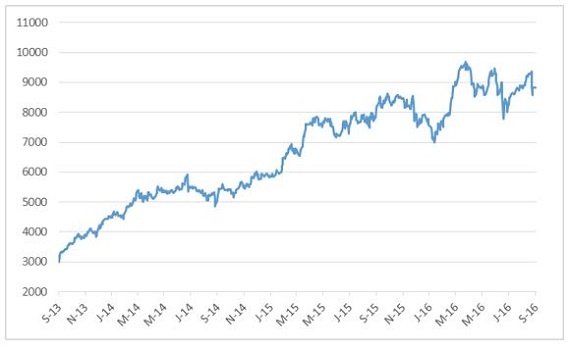

Discovery, Sanlam and Old Mutual based to 100 on 5 September 2013

Home Furnishings

![]()

Share price: R85,79

Net shares in issue: 3761 million

Market cap: R322 billion

Exit PE ratio 15,3x; forward PE 14,0x

Dividend yield 2,2%

Fair value: R75

Target price: R85

Trading Sell and Portfolio Buy

Home furnishings leviathan Steinhoff releases results for the twelve months to June 2016 on Wednesday.

At an extraordinary general meeting, the board approved a change in year end to September and so the financial year in 2016 will be a fifteen month year. However, the twelve month results will give full detail.

Steinhoff gives quarterly updates since the primary listing moved to Frankfurt and did so for Q4, released on 31 August.

Revenue for the twelve months came in at €13 059 million with operating profit before capital items at €1 474 million.

All operations have contributed positively, by and large, in home currencies.

As the Pepkor group was acquired with effect from 31 March 2015, three months of the Pepkor contribution was included in the comparative.

The weakness of the rand chopped €735 million off revenue on a constant currency basis – growth in revenue would have been 41% in euro in constant currency rather than 33%. The rand for the twelve months is translated at R16,12/€ compared with R13,74/€.

In actual currency, South Africa still represents 32% of reported topline but this increases to 36% in constant currency.

However, when it comes to profits I estimate that South Africa will be around 25% of the group when the full detail is published on Wednesday.

I estimate headline earnings from continuing operations for the year ending 30 June 2016 of €1 300 million. This translates to EPS for the year of 35 cents in euro or 564 SA cents. On a 3x dividend cover that means a dividend of about 12 euro cents or 194 SA cents depending on the exchange rate.

As recently discussed in various notes, corporate activity is high on the agenda, including Poundland. If the Mattress Firm deal in the US goes through the combination increases group revenue to €17 billion and EBITDA to €2 billion.

The earnings impact is not quite so large, at least initially.

I estimate Mattress Firm adds 0,7 euro cents on a pro forma basis to earnings compared with my 2016 group estimate of 35 euro cents and thus 2%. I estimate that Poundland could add 0,6 euro cents to earnings on a pro forma basis, after interest on acquisition debt. Combined the pro forma impact is 1,3 euro cents or 3,7% of forecast 2016 earnings.

Going forward, the impact of the acquisitions will be larger as cash flow is generated and debt reduces. The cumulative impact on Steinhoff of acquisitions over the years has been considerable.

There is no further clarity on the German tax investigation. Whilst the outcome is unknowable it could have potential negative valuation consequences, as I’ve cautioned since 2014.

I’ll review estimate post results but meantime I am looking at three-year compound growth in earnings in euro of 10% - excluding corporate action. Currency movements will affect euro reported results.

At a Frankfurt price of €5,46 the rolling exit PE ratio is 15,3x with the gross dividend yield at 2,2%.

The recent retreat in the stock from €6,00 to €5,46 and from R93 to R86 is welcome as it was getting frothy.

I’ve had a fair value of R75 and a target of R85 for some time now. I retain a Trading Sell, continuing to advise accumulation in to weakness, but retain a Portfolio Buy recommendation for those with a longer horizon.

Steinhoff share price in rand

Kind Regards,

Mark N Ingham