All supermarket trolleys are not created equal, and a street turf battle has waged for some years to get more of the consumers’ grocery wallet in hard-pressed times. In the past few years, I’ve cautioned about exposure to Woolworths, seen good earnings upside for Pick n Pay, recommended avoidance of Massmart as the investment case wasn’t appealing, underscored the resilience and advantages of the Spar business model, and, in a note last year, suggested that trolley for trolley it was worth paying more for Shoprite. Today, that remains pretty much the order of things. However, food inflation is declining, which means turnover is difficult to get. Dividend yields too are getting thin and price earnings ratios are stretched. And “defensive” isn’t a sufficient condition for exposure to a share, particularly as grocery isn’t quite as defensive as it appears at face value.

“Trolley for Trolley”

EasyEquities Strategies

Featured sector: Food & Drug Retailers

What you need to know:

Shoprite has become something of a grocery juggernaut, growing volume ahead of peers and even giving the posh folk who shop at Woolies reason to (partially) reconsider. With extra volumes they get better rebates from suppliers like National Brands or Nampak and they get scale advantages from the vast distribution centres.

Checkers is spearheading the assault on the mid to upper income consumer and targeting suburban areas where it is underrepresented. I’ve mentioned before that there is an element of cannibalisation to the Shoprite turf-war strategy, with like-for-like sales going backwards, but so far, the volume gains have masked that.

But I should point out that market share gains are hard won and come in very small increments, as shoppers tend to be quite loyal to their grocer.

Over seven years, Shoprite has only edged market share up from 31% to 32% in 2017, Woolies moved up from 7% to 9% but is now struggling to maintain, Pick n Pay has fallen from 29% to 24%, Spar is down from 28% to 27%, and Massmart has held around 8%. That is only the big five, outside of that 100% total for them all are many feisty independents and spaza stores.

Shoprite, of the big five, has gained the most but it is not all about market share. Pick n Pay is doing things differently, focusing on improving efficiencies and not going for a land grab. The team is focused on execution on a clear modernisation strategy, with profitability of the business well leveraged to small increases in top line.

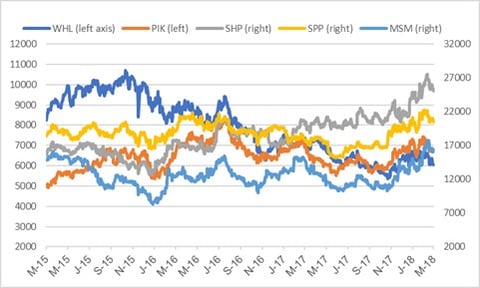

My calls in grocery retail are evident in share price performances this past three years, with Shoprite and Pick n Pay top of the trolley pops and Woolies going backwards, summed up by my recent note entitled “Earnings in Davy Jones’ locker.”

Big fie grocers based to 100 years over three years

Big fie grocers share prices

But, as we have seen with a number of domestic South Africa stocks, local grocery retail is pricey.

Shoprite, on a share price of R255 (ahead of my target level of R225) is on a forward PE ratio of 23x and a yield of only 2,1%, which is 1,7% after dividend withholding tax.

Pick n Pay, at R69, is on a 2018 forward PE ratio of 24x but it is rapidly catching up in earnings and so the 2019 ratio is 19x. Moreover, the dividend yield is relatively more attractive, 2,8% for 2018 and 3,6% for 2019.

I’ve analysed why I would not be exposed to Massmart and Woolies in previous notes, so I won’t labour the point here. Spar, is a possibility as a third choice, assisted by a proven distributor/independent business model and a forward yield that is higher than Shoprite.

In South African grocery, I hold to the view that Pick n Pay has the most ground to make up in earnings, with real growth on the bottom line because of efficiencies but not top line. Overall, Shoprite will grow both top line and bottom line in double digits, helped by other Africa income.

As with all things, you pay your money, you take your choice.

Did you find this note insightful?

Check out previous sector insight: Mind the Gap.

Wishing you profitable investing, until next time.

M N INGHAM