What's been on the rise and fall in the stock market? The team at fund administration and investment management business RISE, unpack it for us.

Over the past few months, we have implored our readers not to be excited about the market recovery that started in October 2022 and framed the rally as a bear market rally in a downward-trending market.

Global Markets

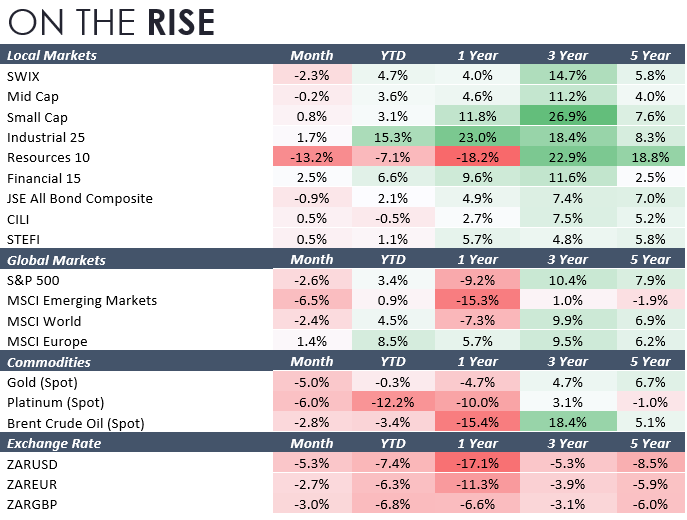

- In February, markets reversed the strong gains experienced in January.

- UK equities held up relatively well in February as economic data showed that the economy is performing more resiliently than expected.

- The Bank of England and European Central bank (ECB) both raised their key interest rate by 0.5%

Local Markets

- After a strong January performance, South African markets experienced a slowdown in February.

Emerging Markets

- In February, emerging markets posted a return of -6.5%, underperforming global peers.

Rand remains weak

- The Rand weakened 5.3% to the dollar in February

In February, markets reversed the strong gains experienced in January. The S&P 500 ended the month down 2.6%, the MSCI World Index ended the month down 2.4%, while the MSCI Europe ended the month down 0.6% and the MSCI Emerging Markets ended the month down 6.5% in USD.

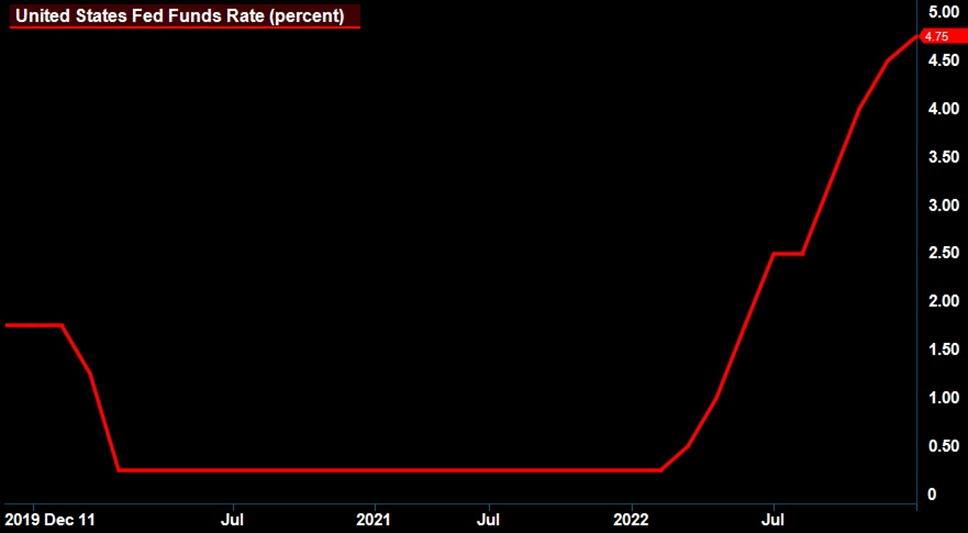

Higher than expected inflation along with robust consumer spending, further added to concerns that the US Fed will not relent in hiking rates until signs of inflation tracking towards to the 2% target are evident. In line with market expectations, the US Federal reserve voted to raise rates by 0.25% to 4.75%. The release of the January US employment report, which showed an increase in employment gains of 517,000, caused market speculators to re-evaluate their stance on the US Fed potentially embarking on rate cuts in the second half of the year.

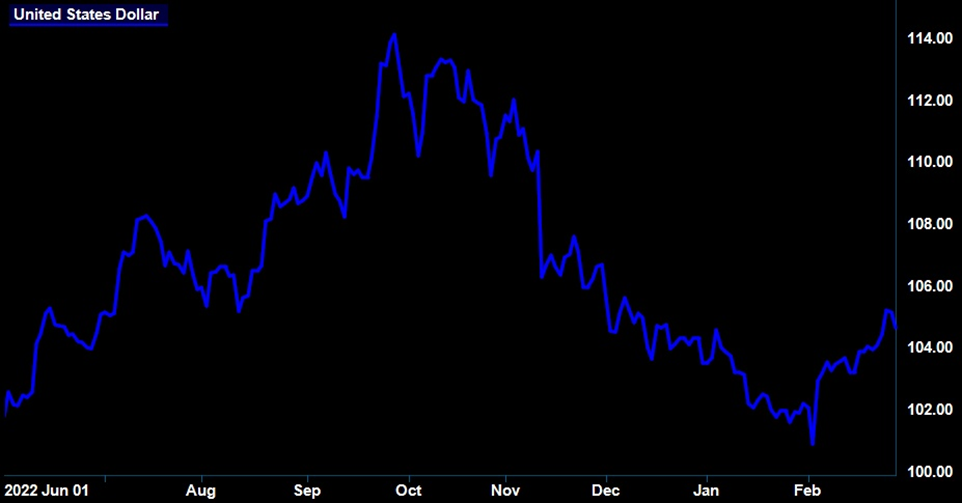

The positive economic data favoured the US Dollar, as it broke its four-month losing streak and closed the month up 2.4%

Chart 1: United States dollar breaks its four-month losing streak.

Chart 2: United States Fed funds Rate

Chart Source: Infront

UK equities held up relatively well in February as economic data showed that the economy is performing more resiliently than expected. GDP data showed that the economy did not contract in the last quarter of 2022, indicating that it has avoided a technical recession after a contraction in the third quarter of 2022. The bank of England however still expects the economy to fall into a recession later in 2023.

The Bank of England and European Central bank (ECB) both raised their key interest rate by 0.5% with a further increase expected in March by the ECB as due to data showing inflation ticking up again in Spain and France.

Emerging Markets

In February, emerging markets posted a return of -6.5%, underperforming global peers. This was partly due to a re-escalation of tensions between the US and China, which dampened market sentiment. In addition, the US released unexpectedly strong macroeconomic data, raising expectations of further interest rate increases. As a result, the dollar strengthened, creating an additional headwind for Emerging markets.

Local Markets

After a strong January performance, South African markets experienced a slowdown in February. The risk-off sentiment rippled through global markets and domestic markets followed suit. The FTSE/JSE SWIX falling by 2.3% MoM, which was largely dragged by weaker commodity prices.

Sector Performance

The resource sector was the hardest hit on the JSE, with a negative return of 13.2%. Resources remain the most volatile sector in the market as global demand dynamics change rapidly. However, Financials and Industrials fared better with both sectors posting positive returns of 2.5% and 1.7% respectively.

Chart Source: Infront, 6 month sector performance

Currency Performance

After a weak January performance, the dollar index regained momentum and ended the month higher in February.

Due to ongoing uncertainty regarding US inflation and the possibility of future short-term interest rate increases, the markets have adopted a risk-off attitude, at least in the short term. As a result, the Rand weakened 5.3% to the dollar in February.

Chart Source: Infront, DXY and ZARUSD 2 year performance

The South African bond market, as indicated by the All-Bond Index (ALBI), decreased by 0.9%. However, the Composite Inflation-Linked Index (CILI), which tracks inflation-linked bonds, increased by 0.5%.

2023 Budget Speech Summary

This month’s domestic economic news was largely focused on Finance Minister Enoch Godongwana’s National Budget Speech.

Overall, it was quite a balanced budget. By that, it strikes a sensible balance between spending/tax relief and fiscal discipline.

Highlights of the 2023 Budget Speech:

- Tax rebates on PV solar panels

In the 2023 SONA, President Cyril Ramaphosa made mention that government will introduce an incentive for solar usage. The incentive is known as the Energy Bounce Back Scheme (to be launched in April 2023), which is as follows:

For individuals – 25% Tax rebate (maximum R15,000 per individual).This, for example, means if solar costs R40,000, the rebate to reduce income tax would be R10,000.

For small and medium enterprises - 20% first loss bases. This means that government takes 20% loss on any default loans for solar and related.

- The State has committed to take on R254 billion worth of ESKOM’s debt over the next three years. While this commitment comes with strict guidelines aimed at improving capacity, the ongoing burden it places on the nation’s fiscal is alarming.

- Tax relief through adjusting the personal income tax brackets and rebates to account for the effect of inflation.

- Extend the COVID-19 social relief of distress grant until 31 March 2024.

- No increase in the general fuel levy.

Despite the initiatives discussed, the government will still achieve a main budget primary surplus in 2022/23. The consolidated budget deficit will decline from 4.6% of GDP in 2021/22 to 4.2% in 2022/23.

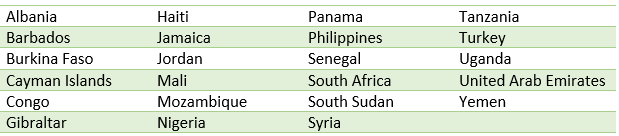

South Africa gets Greylisted

Godongwana spoke about the cloud of greylisting looming over the country. He mentioned that 20 deficiencies had been identified by the Financial Action Task Force (FATF), which is responsible for setting international standards to combat money laundering and terrorism financing across borders.

He added that 15 of these deficiencies will be resolved through the implementation of two legislative acts. The remaining five issues can be addressed through changes in regulations and practices, which do not require legislation. The National Treasury aims to tackle all these deficiencies by January 2025.

What are the implications for a country that is greylisted?

When a country is placed on the greylist, the foremost consequence is the harm it causes to the country's reputation. This is because the country's ability to fight financial crimes such as corruption, money laundering, and terror financing is considered to be inadequate according to international Standards.

When a country goes on this list, it means they have committed to working with the FATF to address issues and is subject to additional scrutiny.

The following is a list of countries on the "Grey list" as of February 2023:

"The accelerating growth (and inflationary pressures) in the US that we have seen over the past two months have put an end to the bear market rally. In March, the Fed further cemented this idea after communicating that faster and more aggressive rate hikes may be needed. Fundamentally, the market environment remains unsupportive of equities – inflation remains elevated, growth is slowing, liquidity is declining and geopolitical risks are high. As a result, we maintain a conservative positioning in our portfolios. Our exposure to global equities is low. Within equities we have taken a more defensive stance, favouring US quality equities and defensive sectors. South African mid and small-cap equities are particularly cheap but vulnerable to a global sell-off. One needs to carefully pick companies that can grow their earnings in a low growth environment.

"Our portfolios have a high allocation to SA Bonds (where longer-dated instruments are still offering double-digit yields) and exposure to commodity backed loans. We also hold a lot of cash in our portfolios. We prefer USD over ZAR given the recent pullback in the dollar index and the countercyclical nature of the dollar. Our large cash position gives us the dry powder we need to take advantage of bargains that may arise from a market sell-offs. Finally, we have a position in renewable energy infrastructure projects, which are not only attractive from an IRR perspective but will meaningfully increase electricity production and reduce carbon emissions in South Africa."

On EasyEquities, there are 12 RISE-managed products across TFSA, RA and EasyZAR. Some of the top-performing bundles year-to-date (YTD) include:

- RISE Growth Passive Fund

- RISE CPI+7

- RISE Moderate Passive Fund

- RISE CPI+5

Compare and view bundles here or below

.jpg?width=1200&length=1200&name=Headphone-man-blog%20(1).jpg)

Sources – Intellidex

Any opinions, news, research, reports, analyses, prices, or other information contained within this research is provided by an external contributor as general market commentary and does not constitute investment advice for the purposes of the Financial Advisory and Intermediary Services Act, 2002. First World Trader (Pty) Ltd t/a EasyEquities (“EasyEquities”) does not warrant the correctness, accuracy, timeliness, reliability or completeness of any information (i) contained within this research and (ii) received from third party data providers. You must rely solely upon your own judgment in all aspects of your investment and/or trading decisions and all investments and/or trades are made at your own risk. EasyEquities (including any of their employees) will not accept any liability for any direct or indirect loss or damage, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on the market commentary. The content contained within is subject to change at any time without notice.