Catch this insight by Intellidex on the The Satrix Property ETF is in Intellidex's view it is the best option for investors seeking diversified exposure to the local property sector. The fund edges its peers on diversification, costs and investment strategy.

Intellidex insight: The Satrix Property ETF is in our view the best option for investors seeking diversified exposure to the local property sector. The fund edges its peers on diversification, costs and investment strategy. Unlike its peers which track the SA Listed Property Index (Sapy), the Satrix Property ETF follows an index created by S&P. The index differs from the Sapy in two important ways.

First, the S&P SA Composite Property Index caps weightings of individual constituents at 10% of the index while the Sapy doesn’t. Largely because of this, the Satrix Property ETF does not suffer from the concentration problem inherent in the Sapy, where just nine of its 20 constituents tend to drive most of the index’s performance. Notably, CoreShares is migrating its two property funds – the CoreShares Proptrax Ten and the CoreShares Proptrax Sapy – away from the Sapy to an inhouse index. This will leave the Stanlib SA Property ETF as the only fund that tracks the Sapy.

Second, unlike the Sapy which is restricted to investing in companies with a primary listing on the JSE, the S&P SA Composite Property Index does not discriminate based on a constituent’s type of listing. Consequently, the Satrix Property ETF tends to have good mix of domestic property companies and some exciting foreign property companies such as Capital Counties, Intu Properties and Hammerson. However, this feature works against the Satrix Property ETF when it comes to its dividend yield because most foreign real estate investment trusts (REITs) tend to have yields which are lower than that of local REITs.

The Satrix Property ETF also beats its rivals on costs. Its total expense ratio of 0.3% is the cheapest, along with that of the Stanlib SA Property ETF.

Fund description: The Satrix Property ETF mimics the value of the S&P SA Composite Property Capped Index. The index modifies the S&P South Africa Composite Property Index to ensure that no single stock takes up more than 10% of the index at each rebalancing.

Click logo to view

Satrix Property ETF

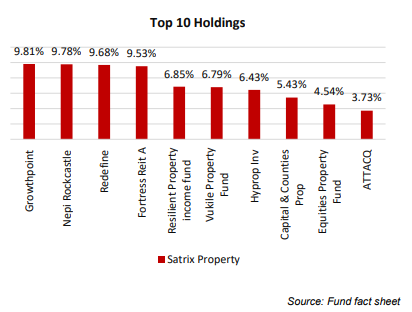

Fund holdings: The Satrix Property ETF’s top 10 holdings constitute 72.6% of its assets. However, due to the 10% cap rule, no single stock dominates. Its funds are fairly distributed across major property stocks on

the JSE. Notably, the Satrix Property ETF has a decent representation of non-SA property companies. In terms of sectors, 42.6% of the fund’s assets are in diversified REITs. Retail REITS account for 27.45%.

Suitability:Due to its sector concentration, the Satrix Property ETF is a bit riskier than a typical broad market fund. As result this fund will suit risk-tolerant investors seeking an income strategy.

Historical performance: The Satrix Property ETF is relatively new in the market —and so far its performance so far has been terrible but in line with developments in the sector.

Fundamentals: Data from the South African Property Owners Association (Sapoa) as well as MSCI’s survey show that occupancy levels in the SA property sector are still decent. Sapoa reported that the national vacancy rate for offices improved to 11% during the third quarter of 2019 from 11.3% in Q2. In the retail sector the vacancy rate of the 100+ shopping centres forming part of the MSCI Retail Trading Density index printed at 4.3% at the end of Q2 2019. The vacancy rate in the industrial sector was at 3.6% at end-2018, which is solid.

However, all sectors reported high rental reversions, which means that lease renewals and new tenant uptakes are coming at lower rental rates. They are also experiencing cost pressures due to high increases in rates, levies and electricity costs. This is constraining REITs’ ability to grow distributions to shareholders. Several companies have since reported declines in dividends. Hyprop, which was a market darling not too long ago, warned that its dividend would drop by between 10% and 13% for its FY20. A Corporate Real Estate, which has been embroiled in a prolonged boardroom battle, also reported below-guidance dividend numbers for the six months to end-June: down 6% versus its earlier forecast of flat growth.

Click logo to view

Satrix Property ETF

We expect this to be the new normal for the sector. SA needs GDP growth of 3.5% or higher to drive employment growth and subsequently demand for space. With the economy not expected to grow anywhere near that level in the short to medium term, it is very difficult to see the sector performing robustly and improving its occupancy levels. The Satrix Property ETF’s decent exposure to rand hedge counters, particularly those exposed to high-growth eastern European markets — such as Nepi Rockcastle, EPP and MAS — will help deflect some of the headwinds facing SA. The outlook for those and other rand hedges are a bit brighter. The looser monetary policy that is prevalent in developed markets also offers some relief to the sector.

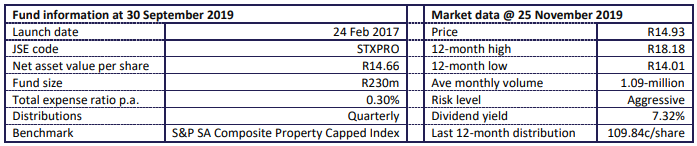

Fund statistics:

Alternatives: CoreShares SA Property Income (TER 0,46) is the only alternative fund to the Satrix Property ETF.

Click below to view

Satrix Property ETF Fact Sheet

Background: Exchange-traded funds (ETFs)

Exchange-traded funds (ETFs) are passively managed investment funds that track the performance of a basket of pre-determined assets. They are traded the same way as shares and the main difference is that whereas one share gives exposure to one company, an ETF gives exposure to numerous companies in a single transaction. ETFs can be traded through your broker in the same way as shares, say, on the Easy Equities platform. In addition, they qualify for the tax-free savings account, where both capital and income gains accumulate tax free.

Benefits of ETFs

- Gain instant exposure to various underlying shares or bonds in one transaction

- They diversify risk because a single ETF holds various shares

- They are cost-effective

- They are liquid – it is usually easy to find a buyer or seller and they trade just like shares

- High transparency through daily published index constituents

|