The CoreShares S&P SA Low Volatility ETF aims to lower the risk of equity investments by investing in stocks with relatively low volatility, a way of measuring risk. Lower volatility stocks tend to have more stable price movements – basically price movements tend to be closer to their long run average. In contrast, high volatility stocks have price movements that jump around the average.

What it does: The CoreShares S&P South Africa Low Volatility ETF tracks the price and yield performance of the S&P SA Low Volatility Index. First, all JSE companies are subjected to the S&P SA Composite Index screening, which selects stocks that meet minimum liquidity and market capitalisation requirements. From those that pass the test, the 40 least volatile stocks are then picked to make up the S&P SA Low Volatility Index, based on the one-year trailing standard deviation. Stocks with steady returns are more likely to make the cut. Among the 40, lower volatility stocks get a bigger waiting than higher volatility stocks.

Invest in CoreShares S&P South Africa Low Volatility ETF

Advantages: Compared with most listed ETFs which limit their universe to the JSE’s top 100 or fewer stocks, this fund has a wider universe which encompasses all JSE-listed stocks (large-, mid- and small-cap stocks) that meet the S&P SA Composite Index criteria.

Suitability: This ETF is likely to makes sense for an investor with a long investment horizon but eager to avoid large swings in the value of her investment.

Performance review: The ETF’s performance has not been very good. The fund grew 7.4% a year since inception in April 2014, which is lower than returns from other common indices such as the all share index, all bond index and property index. The fund has also failed to closely track its underlying index: its tracking error has been consistently above 1%. Most funds on the JSE have tracking errors of less than 0.5%. But the real measure of the fund is whether it has met its objective of having low volatility. The premise for investors is that they may be willing to sacrifice returns in order to avoid the stomach-churning sight of rapid swings in the value of their investment. The fund would prove its worth if it can show an efficient trade-off of risk and return.

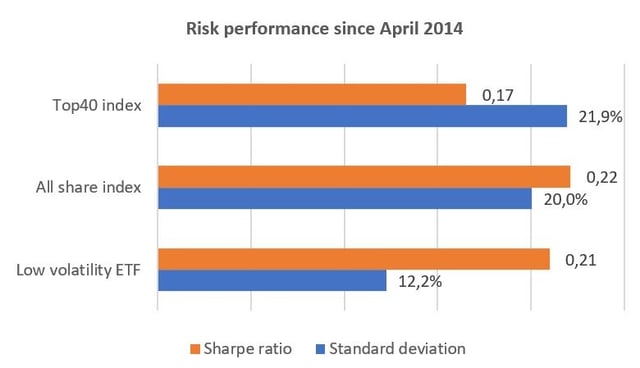

Volatility is defined as the standard deviation of a security’s daily price returns over the prior one year of trading days. Based on standard deviation the fund does perform better than both the top 40 and the all share indices, as it has the lowest standard deviation, which means it has the lowest risk. However, the Sharpe ratio – which measure return per unit of risk – shows that on a risk-adjusted return basis the low volatility fund exhibits inferior returns compared with the all share index, but is better relative to the top 40 index.

.jpg?width=554&height=77&name=16102017(1).jpg)

Fundamental analysis: The CoreShares Low Volatility ETF has not proved to be a popular choice. Despite being more than three years old, it has only R27m in assets under management. In contrast its counterpart, the CoreShares S&P 500 which listed a few months ago, has already attracted more than R425m of assets.

Smart beta/factor-based ETFs such as this one are based on the premise that by shifting away from the traditional market capitalisation-weighted strategy, one can improve the rate of return and/or risk level without getting into expensive and time-consuming stock picking. Low volatility strategies try to ensure that investors don’t face large changes in the value of their investment, but some also claim that they can outperform in price by taking advantage of what is known as the “low volatility anomaly”— the theory that low volatility stocks tend to outperform high-risk stocks over the longer term. The “anomaly” is that the approach departs from traditional financial theory which postulates that by taking on risk, investors can generally expect greater returns.

While there has been a significant body of academic research to support the outperformance of low volatility portfolios, the concept is still not widely accepted. We see two main weaknesses with the strategy:

- For the strategy to work an investor will need a longer than average holding investment period. Research shows that it takes many years for a low volatility portfolio to outperform a high volatility portfolio. Simulations by Wits University found that a low volatility portfolio on the JSE established in 2003 would have overtaken the Swix index only by 2011. Our belief is that such holding periods may not be practically feasible for some investors.

- Unlike market cap filters that favour stocks that are currently performing well, the standard deviation which is used to filter and weight constituents in the low volatility index does not discriminate on the basis of share performance. If two shares move by the same magnitude but in different directions – one up and the other down – they will still have the same standard deviation. This means they will have the same weight in the fund. Stocks with steady returns, regardless of whether they are going up or down, are likely to have a bigger weight in the fund.

.jpg?width=320&name=16102017(2).jpg)

Top holdings: The fund is well diversified with the biggest asset taking up only 4%. This eliminates the idiosyncratic influence of individual stocks, compared with popular market cap-weighted approaches.

Risk: This is a 100% investment in equities, which remains a riskier asset class than bonds or cash. However, potential higher returns over time should compensate for the relatively higher risk.

Fees: The annualised total expense ratio (excluding brokerage and transactional costs) is 0.65%.

.jpg?width=640&name=16102017(3).jpg)

Alternatives: There are no available listed ETFs which track the S&P SA Low Volatility Index. Several other ETFs can provide exposure to equities in general.

Background: Exchange-traded funds (ETFs)

Exchange-traded funds (ETFs) are passively managed investment funds that track the performance of a basket of pre-determined assets. They are traded the same way as shares and the main difference is that whereas one share gives exposure to one company, an ETF gives exposure to numerous companies in a single transaction. ETFs can be traded through your broker in the same way as shares, say, on the EasyEquities platform. In addition, they qualify for the tax-free savings account, where both capital and income gains accumulate tax free.

Benefits of ETFs

- Gain instant exposure to various underlying shares or bonds in one transaction

- They diversify risk because a single ETF holds various shares

- They are cost-effective

- They are liquid – it is usually easy to find a buyer or seller and they trade just like shares

- High transparency through daily published index constituents

If you thought this blog was interesting, you should also read:

Disclaimer

This research report was issued by Intellidex (Pty) Ltd. Intellidex aims to deliver impartial and objective assessments of securities, companies or other subjects. This document is issued for information purposes only and is not an offer to purchase or sell investments or related financial instruments. Individuals should undertake their own analysis and/or seek professional advice based on their specific needs before purchasing or selling investments. The information contained in this report is based on sources that Intellidex believes to be reliable, but Intellidex makes no representations or warranties regarding the completeness, accuracy or reliability of any information, facts, estimates, forecasts or opinions contained in this document. The information, opinions, estimates, assumptions, target prices and forecasts could change at any time without prior notice. Intellidex is under no obligation to inform any recipient of this document of any such changes. Intellidex, its directors, officers, staff, agents or associates shall have no liability for any loss or damage of any nature arising from the use of this document.

Remuneration

The opinions or recommendations contained in this report represent the true views of the analyst(s) responsible for preparing the report. The analyst’s remuneration is not affected by the opinions or recommendations contained in this report, although his/her remuneration may be affected by the overall quality of their research, feedback from clients and the financial performance of Intellidex (Pty) Ltd.

Intellidex staff may hold positions in financial instruments or derivatives thereof which are discussed in this document. Trades by staff are subject to Intellidex’s code of conduct which can be obtained by emailing mail@intellidex.coza.

Intellidex may also have, or be seeking to have, a consulting or other professional relationship with the companies mentioned in this report.